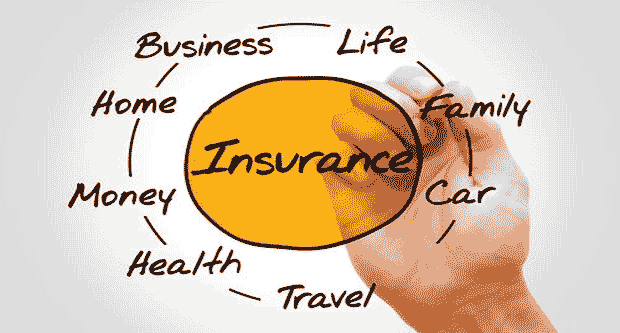

Question: What are the types of insurance?

Insurance comes in many forms, each designed to protect against different types of risks. Here are some common types of insurance, explained through relatable stories.

Auto Insurance

Story: John, a 28-year-old sales manager, was driving to work when he was involved in a minor car accident. The other driver ran a red light and hit John’s car. Thankfully, no one was hurt, but both cars were damaged. John’s auto insurance covered the repair costs for his vehicle and also protected him against any claims from the other driver.

Explanation: Auto insurance provides financial protection against physical damage or bodily injury resulting from traffic collisions. It can also cover theft, vandalism, and natural disasters. Most policies include liability coverage, collision coverage, and comprehensive coverage.

Aviation Insurance

Story: Sarah, a 45-year-old private pilot, was flying her single-engine aircraft on a weekend trip when she encountered unexpected turbulence. The rough air caused minor damage to the plane’s landing gear during descent. Fortunately, Sarah had aviation insurance, which covered the cost of repairs and ensured her aircraft was ready to fly again quickly.

Explanation: Aviation insurance provides financial protection for owners and operators of aircraft against damages or losses due to accidents, weather, or other unforeseen events. It typically includes hull coverage for the aircraft itself, liability coverage for third-party injuries or property damage, and coverage for passengers. Aviation insurance is essential for safeguarding both aircraft and those involved in aviation activities.

Boat Insurance

Story: Jake, a 45-year-old sailing enthusiast, owned a small yacht. During a storm, his yacht was damaged while docked. His boat insurance covered the repair costs, allowing Jake to get back on the water without incurring significant expenses.

Explanation: Boat insurance provides coverage for watercraft against risks like damage, theft, and liability. It helps boat owners manage repair or replacement costs and protects them against liability claims arising from boating accidents.

Business Insurance

Story: David, a small business owner, ran a popular café. One day, a customer slipped and fell inside the café, leading to a lawsuit. David’s business insurance policy covered the legal fees and the settlement, allowing him to continue operating without major financial strain.

Explanation: Business insurance provides coverage for various risks faced by businesses, including property damage, liability claims, and business interruptions. It helps protect the financial health of the business and ensures continuity in case of unforeseen events.

Contractors All Risk (CAR) Insurance

Story: Emma, a 35-year-old construction company owner, was in the middle of a major building project when a severe storm hit the site. The storm caused significant damage to the partially constructed building and some of the machinery. Fortunately, Emma had Contractors All Risk (CAR) insurance, which covered the costs of the repairs and the lost materials, allowing the project to continue without incurring substantial financial losses.

Explanation: CAR insurance provides comprehensive coverage for construction projects, protecting against physical loss or damage to the construction works, plant, equipment, and materials. It also covers third-party liabilities arising from construction activities, ensuring that contractors can manage risks effectively.

Cyber Insurance

Story: Alex, a 42-year-old IT professional, owned a small tech company. One day, his company fell victim to a cyberattack, leading to a data breach and financial losses. His cyber insurance policy covered the costs of investigating the breach, notifying affected clients, and restoring the compromised data.

Explanation: Cyber insurance protects businesses against losses resulting from cyberattacks, data breaches, and other cyber threats. It covers expenses such as data recovery, legal fees, and notification costs, helping businesses recover from cyber incidents.

Disability Insurance

Story: Tom, a 45-year-old construction worker, suffered a severe back injury that left him unable to work for several months. His disability insurance provided him with a portion of his income during his recovery, helping him manage household expenses and medical bills.

Explanation: Disability insurance offers income protection if you are unable to work due to illness or injury. It helps cover living expenses and maintain financial stability when you cannot earn your regular income.

Engineering Insurance

Story: Lisa, a 40-year-old project manager, was overseeing the construction of a new office building. During the construction, a crane malfunctioned, causing extensive damage to the building structure. The engineering insurance policy covered the repair costs and the losses incurred due to the delay, allowing the project to continue without major financial setbacks.

Explanation: Engineering insurance covers a wide range of risks associated with engineering projects, including construction and machinery breakdowns. It provides financial protection against damages and losses, ensuring that projects can proceed smoothly and efficiently despite unexpected issues.

Erection All Risks (EAR) Insurance

Story: John, a 42-year-old engineer, was responsible for installing a new manufacturing plant. During the installation, a critical component was accidentally damaged, delaying the project. John’s Erection All Risks (EAR) insurance policy covered the repair costs and the losses due to the delay, allowing the project to be completed without significant financial strain.

Explanation: EAR insurance covers risks associated with the erection, installation, and testing of machinery, plants, and equipment. It provides financial protection against physical loss or damage and third-party liability, ensuring that projects can be completed on time and within budget.

Flood Insurance

Story: Nina, a 30-year-old homeowner, lived in a flood-prone area. One year, a severe storm caused the nearby river to overflow, flooding her home. Thankfully, Nina had flood insurance, which covered the cost of repairing her home and replacing damaged belongings.

Explanation: Flood insurance covers damage to properties and belongings caused by flooding. It is typically required in flood-prone areas and provides financial protection against flood-related losses, which are not covered by standard homeowners insurance.

Health Insurance

Story: Sarah, a 35-year-old graphic designer, suddenly fell ill and was diagnosed with appendicitis. She needed surgery immediately. Thanks to her health insurance, Sarah’s medical bills, including surgery, hospital stay, and post-operative care, were mostly covered. Without health insurance, the cost would have been overwhelming.

Explanation: Health insurance covers medical expenses such as doctor visits, hospital stays, surgeries, and prescription medications. It helps manage the high costs of healthcare and ensures access to necessary treatments without financial strain.

Homeowners Insurance

Story: Emily and Jack had just bought their dream home. A few months later, a severe storm caused a tree to fall on their roof, leading to significant damage. Their homeowners insurance policy covered the cost of repairs, preventing a major financial setback.

Explanation: Homeowners insurance protects against damages to your home and personal property due to events like fire, theft, vandalism, and natural disasters. It also provides liability coverage if someone is injured on your property.

Life Insurance

Story: Mike, a 40-year-old father of two, wanted to ensure his family would be financially secure if anything happened to him. He purchased a life insurance policy. Tragically, Mike passed away in an accident a few years later. The life insurance payout helped his family cover living expenses, pay off debts, and secure his children’s education.

Explanation: Life insurance provides a financial payout to beneficiaries upon the policyholder’s death. It helps cover expenses such as funeral costs, outstanding debts, and living expenses for the surviving family members, ensuring financial stability during a difficult time.

Long-Term Care Insurance

Story: Martha, a 70-year-old retiree, developed a chronic illness that required long-term care. Her long-term care insurance policy covered the costs of her nursing home care, reducing the financial burden on her family and ensuring she received the necessary care.

Explanation: Long-term care insurance covers the costs associated with long-term care services, such as nursing home care, assisted living, and in-home care. It helps individuals manage the high costs of long-term care without depleting their savings.

Machinery Breakdown Insurance

Story: Sophie, a 50-year-old factory owner, faced a major setback when her main production machine suddenly broke down. The repair costs were substantial, and the production halt threatened to cause significant financial losses. However, Sophie’s Machinery Breakdown insurance covered the repair expenses and provided compensation for the lost income during the downtime, helping her get the factory back to full operation quickly.

Explanation: Machinery Breakdown insurance provides coverage for the sudden and accidental breakdown of machinery and equipment. It covers the repair or replacement costs and any consequential financial losses due to the machinery’s downtime, ensuring that businesses can recover swiftly from equipment failures.

Marine Insurance

Story: Tom, a 45-year-old shipping company owner, had a cargo ship transporting goods overseas. During a storm, the ship encountered rough seas, and some of the cargo was damaged. The marine insurance policy covered the loss, compensating Tom for the damaged goods and allowing his business to continue without significant financial loss.

Explanation: Marine insurance covers the loss or damage of ships, cargo, and other maritime assets during transport. It provides financial protection for shipping companies and cargo owners, ensuring that they can recover from losses due to maritime risks like storms, collisions, and piracy.

Pet Insurance

Story: Lila, a 30-year-old veterinarian, adopted a puppy named Max. One day, Max swallowed a small toy and needed emergency surgery. Lila’s pet insurance covered most of the veterinary expenses, ensuring Max received the best care without a significant financial burden.

Explanation: Pet insurance helps cover veterinary costs for your pets. It includes coverage for accidents, illnesses, surgeries, and sometimes routine care. It ensures that your pets receive the necessary medical attention without causing financial stress.

These stories illustrate how different types of insurance provide protection and peace of mind in various aspects of life, helping individuals and families manage unexpected events and financial challenges.

Property Insurance

Story: Karen, a 50-year-old homeowner, experienced a devastating fire that severely damaged her house. Her property insurance covered the costs of repairing the damaged sections of her home and replacing the lost belongings, enabling her to rebuild and recover from the disaster.

Explanation: Property insurance provides coverage for buildings and their contents against risks like fire, theft, and natural disasters. It helps homeowners and businesses manage the costs of repairing or replacing damaged property, ensuring financial stability after an unexpected event.

Renters Insurance

Story: Jessica, a 26-year-old teacher, rented an apartment in the city. One night, a fire in the neighboring apartment spread, causing smoke damage to Jessica’s belongings. Her renters insurance covered the cost of replacing her damaged items, making the recovery process much easier.

Explanation: Renters insurance protects the personal belongings of tenants against risks like fire, theft, and vandalism. It also provides liability coverage if someone is injured in the rental property. It ensures that renters can recover their losses without significant financial hardship.

Travel Insurance

Story: Anna and Mark planned a dream vacation to Europe. A week before their departure, Anna fell and broke her leg, making it impossible for them to travel. Their travel insurance reimbursed them for the non-refundable trip expenses, allowing them to plan another vacation once Anna recovered.

Explanation: Travel insurance covers various risks associated with travel, including trip cancellations, medical emergencies, lost luggage, and travel delays. It provides peace of mind and financial protection when unexpected events disrupt travel plans.

Umbrella Insurance

Story: Chris, a 50-year-old homeowner, was involved in a car accident where he was at fault, causing significant injuries to the other driver. The medical bills and damages exceeded his auto insurance liability limits. Fortunately, his umbrella insurance provided additional liability coverage, protecting his assets from being seized to cover the costs.

Explanation: Umbrella insurance provides additional liability coverage beyond the limits of other policies, such as auto or homeowners insurance. It offers extra protection against large claims or lawsuits, safeguarding your assets and financial future.

Workers’ Compensation Insurance

Story: Emma, a 35-year-old construction worker, injured her back while lifting heavy materials at work. Her employer’s workers’ compensation insurance covered her medical expenses and provided her with a portion of her wages while she was unable to work, helping her recover without financial stress.

Explanation: Workers’ compensation insurance provides benefits to employees who suffer work-related injuries or illnesses. It covers medical expenses, rehabilitation costs, and a portion of lost wages, ensuring that employees receive support during their recovery.

These stories further illustrate how various types of insurance provide protection and peace of mind in different aspects of life, helping individuals, families, and businesses manage unexpected events and financial challenges.