Question: What is the impact of behavioral finance on investment decisions?

Behavioral finance has emerged as a critical field in understanding how psychological factors and biases influence investors’ decisions and financial market outcomes. Traditional financial theories often assume that investors are rational and markets are efficient. However, behavioral finance challenges this notion by highlighting how emotions, cognitive errors, and social influences can lead to irrational financial behaviors. This article explores the key concepts of behavioral finance, the common biases that affect investment decisions, and their implications for financial markets.

Understanding Behavioral Finance

Behavioral finance is a field of study that combines psychology and economics to explain why and how investors make financial decisions. It seeks to understand the effects of psychological, social, cognitive, and emotional factors on the economic decisions of individuals and institutions. Behavioral finance posits that investors are not always rational and are influenced by their own biases and emotions.

Key Concepts in Behavioral Finance

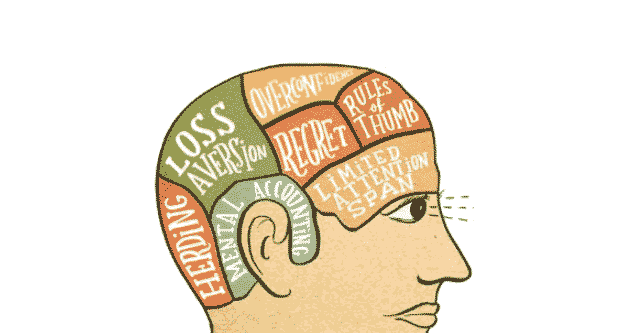

- Heuristics: Heuristics are mental shortcuts or rules of thumb that people use to make decisions quickly. While they can be useful, they often lead to biased or suboptimal decisions.

- Prospect Theory: Developed by Daniel Kahneman and Amos Tversky, prospect theory suggests that people value gains and losses differently, leading to decisions that deviate from expected utility theory. For example, investors may exhibit loss aversion, where the pain of losing is greater than the pleasure of gaining.

- Overconfidence: Investors often overestimate their knowledge, abilities, and the accuracy of their predictions. This overconfidence can lead to excessive trading and risk-taking.

- Anchoring: Anchoring refers to the tendency to rely too heavily on the first piece of information encountered (the “anchor”) when making decisions. This can cause investors to make irrational choices based on initial figures or data points.

Common Biases in Investment Decisions

Behavioral finance identifies several common biases that can influence investment decisions. Understanding these biases can help investors recognize and mitigate their effects.

1. Confirmation Bias

Confirmation bias is the tendency to search for, interpret, and remember information in a way that confirms one’s preexisting beliefs or hypotheses. Investors with confirmation bias may seek out information that supports their investment choices while ignoring or downplaying information that contradicts them. This can lead to poor decision-making and reinforce erroneous beliefs.

2. Herding Behavior

Herding behavior occurs when investors follow the actions of a larger group, often leading to collective irrationality. This can result in market bubbles and crashes, as investors buy or sell assets based on the actions of others rather than their own analysis. Herding is driven by the fear of missing out (FOMO) and the desire for social conformity.

3. Loss Aversion

Loss aversion is the tendency to prefer avoiding losses rather than acquiring equivalent gains. For example, losing $100 is typically more distressing than gaining $100 is satisfying. This bias can cause investors to hold onto losing investments for too long in the hope of breaking even, or to sell winning investments too early to lock in gains. It is also known as regret aversion bias.

4. Mental Accounting

Mental accounting refers to the tendency to treat money differently depending on its source or intended use. Investors might allocate funds into separate “mental accounts” for specific purposes, leading to irrational investment decisions. For instance, they might be more willing to take risks with “house money” (profits from previous investments) than with their initial capital.

5. Anchoring Bias

Anchoring bias occurs when investors fixate on a particular reference point, such as a past stock price, and use it as a benchmark for future decisions. This can lead to irrational investment behavior, as the anchor may not be relevant to current market conditions. Anchoring can cause investors to hold onto losing stocks in the hope of a return to a previous high or to sell winning stocks prematurely.

6. Negativity Bias

Negativity bias is the tendency to give more weight to negative information or experiences than positive ones. This bias can lead investors to become overly pessimistic, focusing on potential losses and risks while overlooking opportunities for gains. As a result, they may miss out on lucrative investments due to an excessively cautious approach. For instance, an investor might avoid investing in a stock with strong growth potential because of negative news reports, despite positive long-term prospects. Recognizing and mitigating negativity bias can help investors make more balanced and informed decisions.

7. Recency Bias

Recency bias occurs when recent events heavily influence our decisions, causing us to overlook historical data. This bias leads investors to place disproportionate importance on recent market trends, often at the expense of long-term perspectives. For instance, during the COVID-19 pandemic in March 2020, equity markets plunged, and investors panicked, forgetting previous market recoveries, such as after the 2008 financial crisis and the 1992 stock market crash. Despite historical evidence of recovery, many investors succumbed to recency bias, making decisions driven by immediate market conditions.

8. Sunk Cost Fallacy

The sunk cost fallacy refers to the tendency to continue investing in a project or asset based on the cumulative prior investment (time, money, effort) rather than its current and future potential. Investors affected by this bias may hold onto underperforming assets, hoping to recover their losses, rather than reallocating resources to more promising opportunities. This behavior can result in prolonged financial underperformance. For example, an investor might keep funding a struggling business venture because of the significant resources already invested, even when it would be wiser to cut losses and move on.

9. Overconfidence Bias

Overconfidence bias occurs when investors overestimate their knowledge and abilities, leading them to make risky investment decisions. This bias can result in excessive trading and a failure to adequately assess risks. Overconfident investors often believe they can predict market movements accurately, which can lead to significant financial losses. Maintaining an open mind and acknowledging the limits of one’s knowledge is crucial for making informed investment choices.

10. Disposition Effect Bias

Disposition effect bias refers to the tendency to classify investments as “winners” or “losers,” often leading to suboptimal decision-making. Investors might hold onto underperforming assets, hoping for a turnaround, or sell winning investments too early to realize gains. This behavior can increase capital gains taxes and reduce overall returns. To counteract this bias, investors should evaluate each investment based on its current and future potential rather than past performance.

11. Hindsight Bias

Hindsight bias is the tendency to believe, after an event has occurred, that its outcome was predictable and obvious, even though it wasn’t. This bias can lead investors to overestimate their ability to predict market movements, fostering overconfidence and potentially risky behavior. Recognizing the unpredictability of markets and avoiding hindsight bias can help investors maintain a realistic perspective on their forecasting abilities.

12. Familiarity Bias

Familiarity bias occurs when investors prefer familiar investments, often at the expense of diversification. This bias can lead to a concentration in domestic or well-known securities, ignoring potentially profitable opportunities in less familiar markets. By overcoming familiarity bias and embracing diversification, investors can build more robust and balanced portfolios, reducing risk and enhancing returns.

13. Self-attribution Bias

Self-attribution bias is the tendency to attribute positive outcomes to one’s actions and negative outcomes to external factors. This bias can lead to overconfidence and a distorted view of one’s investment skills. Investors affected by self-attribution bias may take undue credit for successful investments while blaming external factors for failures. Acknowledging the role of luck and external influences in investment performance can help maintain a more balanced and realistic perspective.

14. Trend-chasing Bias

Trend-chasing bias is the tendency to invest based on past performance, mistakenly believing that historical returns will predict future outcomes. This behavior can be exacerbated by increased advertising from financial product issuers during periods of strong performance. Research shows that past performance often fails to persist, and trend-chasing can lead to poor investment decisions. Investors should focus on fundamental analysis and long-term strategies rather than chasing short-term trends.

The Impact of Behavioral Biases on Financial Markets

Behavioral biases not only affect individual investors but also have significant implications for financial markets as a whole. These biases can lead to market inefficiencies, such as mispricing of assets, bubbles, and crashes.

Market Bubbles and Crashes

Herding behavior and overconfidence can contribute to the formation of market bubbles, where asset prices rise significantly above their intrinsic value. When investors collectively buy into the hype, prices can become inflated. Eventually, when the bubble bursts, a market crash occurs as investors panic and sell off their assets, often exacerbating the decline.

Mispricing of Assets

Behavioral biases can lead to the mispricing of assets, as investors’ decisions are influenced by emotions and cognitive errors rather than fundamental analysis. For example, overconfidence can result in the overvaluation of certain stocks, while loss aversion can lead to the undervaluation of others. These mispricings create opportunities for informed investors to exploit market inefficiencies.

Volatility

Behavioral biases can increase market volatility as investors react to news and events in unpredictable ways. For instance, anchoring bias can cause sudden price swings when new information contradicts investors’ initial beliefs. Similarly, confirmation bias can lead to overreactions to positive or negative news, amplifying market movements.

Mitigating the Impact of Behavioral Biases

While it is challenging to eliminate behavioral biases entirely, investors can take steps to mitigate their impact on decision-making and improve their investment outcomes.

Diversification

Diversifying investments across different asset classes, sectors, and geographies can help reduce the impact of individual biases. A diversified portfolio is less likely to be influenced by the irrational behavior of investors in a particular market segment.

Systematic Investing

Implementing systematic investing strategies, such as dollar-cost averaging or following a disciplined investment plan, can help investors avoid making impulsive decisions based on emotions or market noise. These strategies promote consistent, long-term investing and reduce the likelihood of timing the market incorrectly.

Education and Awareness

Increasing awareness and education about behavioral finance can help investors recognize their own biases and make more informed decisions. By understanding the psychological factors that influence their behavior, investors can take proactive steps to counteract them.

Seeking Professional Advice

Consulting with financial advisors or using robo-advisors can provide an objective perspective and help mitigate the impact of behavioral biases. Professional advisors can offer guidance based on fundamental analysis and long-term investment strategies, reducing the influence of emotions on decision-making.

Conclusion

Behavioral finance provides valuable insights into the psychological factors and biases that influence investors’ decisions and financial market outcomes. By understanding and recognizing these biases, investors can take steps to mitigate their impact and improve their investment performance. The field of behavioral finance highlights the importance of education, diversification, and systematic investing in navigating the complexities of the financial markets. As investors become more aware of their own behavioral tendencies, they can make more rational and informed decisions, ultimately contributing to more efficient and stable financial markets.